The Internet’s geography is changing. Companies of all sizes are deploying more network and computing infrastructure to reach more people around the world more directly. In some cases, this infrastructure is built to improve performance and cut network backhaul costs. In others, it is being built in response to growing numbers of people and businesses connecting, driving demand for digital services, and producing copious amounts of data that is stored and analyzed.

The development of the world’s Internet infrastructure landscape has historically taken its cue from other more established industries, such as the financial services and logistics verticals. These industries have been known to generate economies of scale through centralizing their core ecosystem within a few select global markets. For financial services, the London, Singapore, Hong Kong, Tokyo, Frankfurt, and New York markets have long been seen as the top financial and economic hubs in the world. Those markets, therefore, have also been natural logistics, import, and export hubs, given how the flow of capital impacts industries that are especially capital intensive.

As the Internet infrastructure landscape continues to mature and experience both sustained and accelerating levels of adoption and usage on a global scale, the benefits of centralization now come with certain glaring weaknesses in resiliency, redundancy, performance, and regulatory perspective. These factors have driven a new wave of investments and development activity outside of the traditional, global Tier 1 markets that are now experiencing elevated levels of land and power constraints given the high level of population density residing within these economic and infrastructure hubs.

And that’s why emerging markets in Southeast Asia (the Philippines, Indonesia, Malaysia, Thailand, and Vietnam) are all being bullishly positioned as a prime destination for the next wave of digital infrastructure deployments and investments in the APAC region.

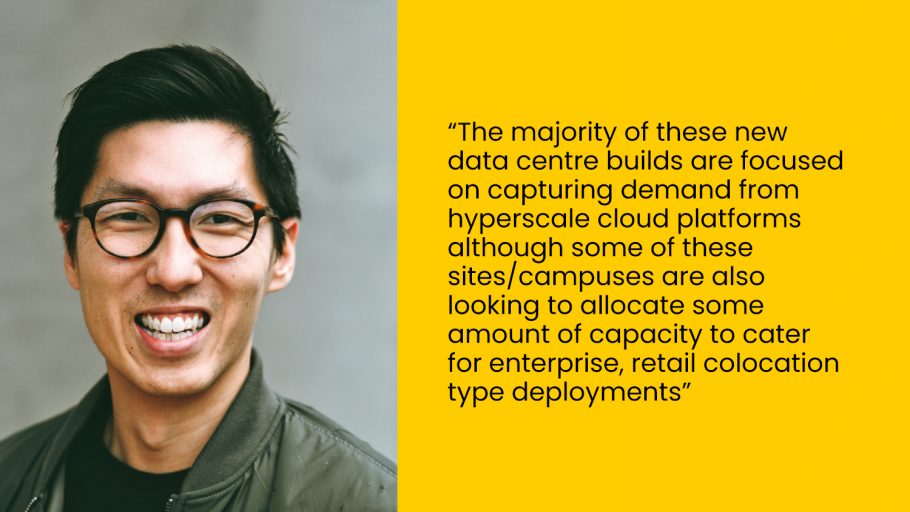

Hyperscale cloud infrastructure deployments in the APAC region are quickly moving into the second tier of markets listed above, and Southeast Asia is leading the way, given it has the highest concentration of emerging economies in the region. Singapore is already the region’s established hub, but the likes of Malaysia, Thailand, the Philippines, and Vietnam all have real growth potential, and are currently at various stages of development. ut it is Indonesia that is far and away the market with the largest upside potential, and the momentum in Jakarta over the last few years speaks to this reality.

Jakarta, Indonesia

Indonesia is the fourth largest country in the world by population and is now home to a burgeoning tech startup community that is serving a country jumping online at a frantic pace. The combination of unique linguistic and cultural characteristics, and tremendous scale, has enabled Indonesia to build homegrown Internet economy services. Indonesia is now home to nearly a dozen unicorns, and basically all of them are running on public cloud infrastructure. To support this growth, hyperscale cloud providers need large quantities of data centre capacity and have been aggressively leasing hyperscale colocation as a result.

The Jakarta data centre colocation market continued to push forward during the pandemic and is projected to be worth 336.6 million USD in 2022. The sector will grow steadily at a five-year CAGR of 22.7 percent through 2027, with hyperscale as the primary driver.

Investors and operators expect demand and absorption to trend aggressively, and inventory is being built while land banks are being rapidly assembled in anticipation of the growth to come. On a MW basis, total data centre colocation inventory in Jakarta is expected to grow at a five-year CAGR of 28 precent, with the hyperscale and wholesale inventory portion growing at a much higher five-year CAGR of 39 percent.

ABOUT THE AUTHOR

Jabez Tan is Head of Research at Structure Research, an independent research and consulting firm devoted to the cloud and data center infrastructure services markets, particularly in the hyperscale value chain. He specializes in the data center infrastructure market and leads both coverage of the APAC region and the building of Structure Research’s proprietary market share data.